Withholding personal income tax in 1C: Accounting 8.3

The calculation and withholding of personal income tax is carried out by the employer in accordance with Article 23 of the Tax Code of the Russian Federation. Because Many organizations use the 1C: Accounting 8.3 program for accounting, let’s take a closer look at the settings and documents necessary to correctly reflect personal income tax transactions.

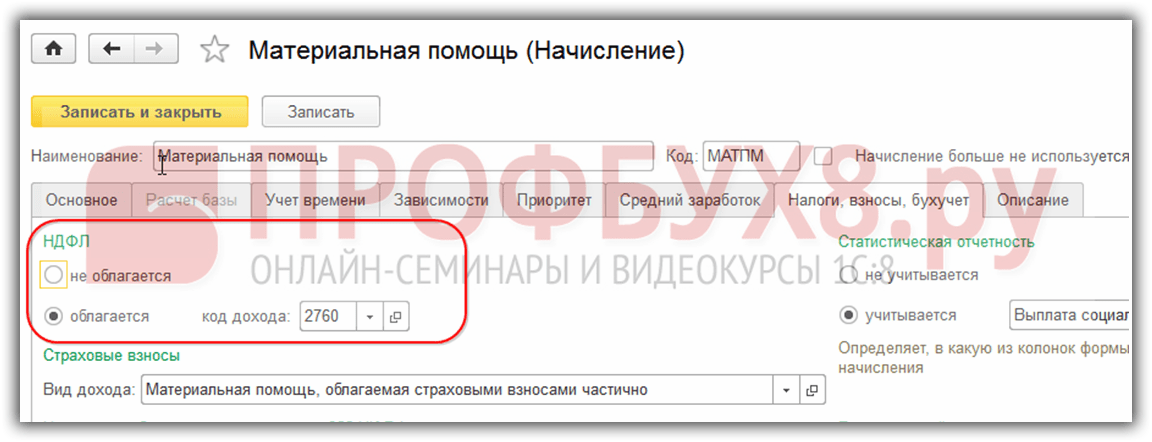

First, let’s turn to the system settings and consider which charges will be subject to personal income tax. To do this, you need to follow the navigation path: Salaries and personnel / Salary settings / Accruals.

For each type of accrual, personal income tax withholding settings are set. Accordingly, when the “Taxed” switch is selected, the tax will be automatically calculated for this accrual.

The income code is selected from the regulated directory “Types of Personal Income Tax”, where the tax rate and additional settings for applying deductions are indicated.

Following the navigation path Main / Settings / Taxes and reports / Personal Income Tax, a setting is set for the correct accounting of tax deductions “On a cumulative basis during the tax period”.

Additionally, the employee’s card contains personalized tax information. The directory is located along the path: Salaries and personnel / Personnel records / Employees; to fill out, you must follow the link in the “Income Tax” field.

- standard child tax credit;

- property deductions;

- social deductions.

Also, the person responsible for reflecting documents indicates the taxpayer status (the default is “resident”) and income from the previous place of work.

Tax calculation in the program is fully automated. When conducting accrual documents, personal income tax amounts are calculated for employees, and also take into account various types of tax deductions. Let's move along the path Salaries and personnel / All accruals to the main payroll document. In the “Personal Income Tax” column, fill in the tax amounts calculated from the amount in the “Accrued” column, taking into account the tax rate for the employee.

By clicking on the tax amount in the line, the user goes to the detailed calculation form, where summary information on the employee is available to check the correctness of the amounts.

Personal income tax withholding is also carried out in the following documents:

- "Vacation";

- "Sick leave";

- "Dismissal";

- and other intersettlement documents.

To analyze accrued amounts, it is recommended to use the “Personal Income Tax Analysis by Month” report, located along the path: Salaries and Personnel / Salary / Personal Income Tax Analysis by Month. In the report window that opens, you must specify the organization, the “Details by employees” flag if grouping by employees is necessary, and set the analyzed period:

Also a convenient form for analysis is the report “Summary certificate 2-NDFL”, presented in a similar section. This report contains brief information displayed in 2-NDFL certificates and is often used to reconcile amounts.

Still have questions? We will help you with withholding personal income tax in 1C 8.3 as part of a free consultation!

To correctly account for personal income tax in the 1C ZUP 8.3 (3.0) program, let's start with the basic settings.

Step 1. Accounting policy for personal income tax

Settings – Organizations (or Organization details) – Accounting policies:

Step 2. Personal income tax deductions

Section Taxes and contributions - Types of personal income tax deductions:

The amounts of deductions provided are stored in each type of deduction. If you notice that the wrong deduction amount is used when calculating personal income tax, you can check it by opening the type of personal income tax deduction of interest:

In order for the amounts of deductions in the 1C 8.3 ZUP database to comply with the law, it is necessary to maintain the working configuration in the current release, that is, regularly update it.

At the same time, the procedure for applying standard tax deductions and setting personal income tax accounting parameters can be studied in the following video:

Step 3. Income subject to personal income tax

You can check which income in the 1C 8.3 ZUP program is included in the tax base and with which code in two ways:

- Open the Taxes, contributions, accounting tab in the accrual document (Settings – Accruals):

- Open the list of accruals (Settings – Accruals) and use the button Setting up personal income tax, average earnings, etc.:

Step 4. Taxpayer information

Step 4. Taxpayer information

The following data is entered through the employee’s card using the “Income Tax” link:

- Taxpayer status;

- Standard, property and social deductions;

- Notice of Advance Payments for Patents;

- Certificate of income from previous employer:

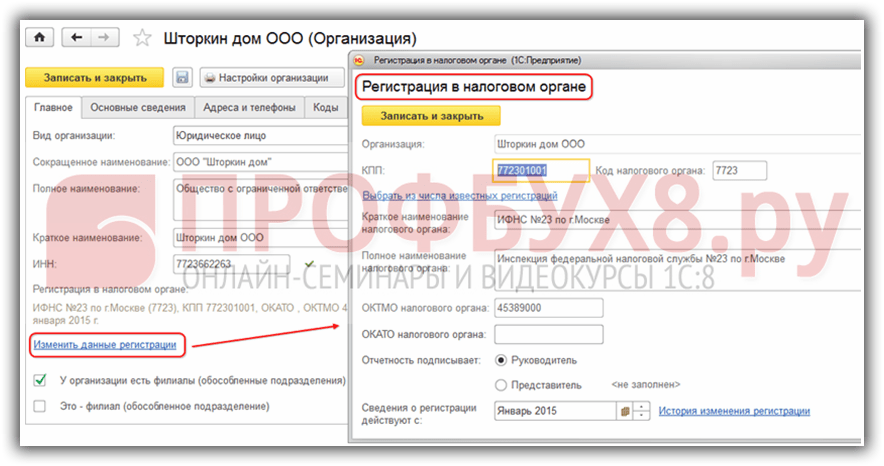

Step 5. Registration with the tax authority

An organization, as a tax agent, provides personal income tax reporting at the place of registration of the organization or at the place of registration of separate divisions to the tax authority.

In the 1C 8.3 Salary and Personnel Management program, registration with the tax authority can be configured according to the appropriate types.

Important! The unit must have the attribute “This is a separate unit”:

If an organization needs to keep records by territory, then this functionality must first be included in the organization’s accounting policy:

Then create a territory (Settings – Territories) and indicate which Federal Tax Service it is registered with:

Calculation of personal income tax in 1C ZUP 8.3 using an example

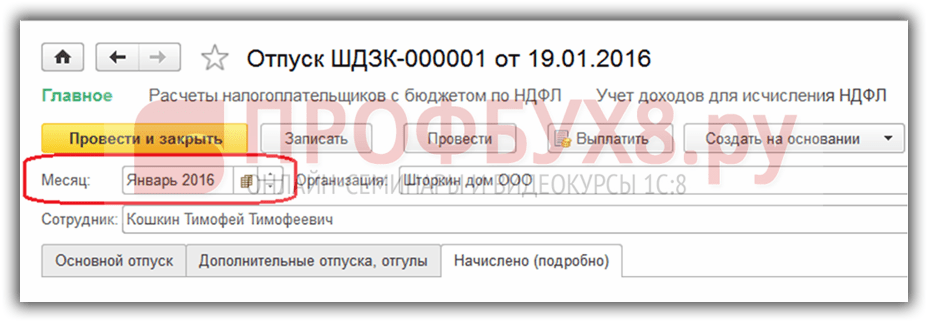

Personal income tax is calculated in 1C 8.3 ZUP 3.0 in documents such as Payroll and contributions, Vacation, Sick leave, etc. Let's look at the calculation of personal income tax using the example of vacation accrual.

To do this, create a Vacation document:

The document contains the calculation of personal income tax. In our example, personal income tax amounted to RUB 2,768.00.

How personal income tax reporting is generated in 1C 8.3 ZUP 3.0

When posting the Vacation document, an entry is made into the accumulation registers. Based on these registers, various personal income tax reports are generated, including a 2-NDFL certificate and a 6-NDFL calculation. These are the registers:

- Register “Accounting for income for calculating personal income tax”;

- Register “Calculations of taxpayers with the budget for personal income tax”;

- Register “Provided standard and social deductions (NDFL)”.

How to view entries in accumulation registers during accrual

You can see the entries made by the “Vacation” document in the navigation panel of the form. By default, the user does not see this panel.

Let's set it up. To do this, while in an open document, select Main Menu – View – Setting the Form Navigation Panel:

The Navigation Panel Settings window opens. In the Available commands section, you must select the register by which you want to view the movements, that is, the entries made by the 1C 8.3 ZUP program when posting the document. Then click the Add button.

For example, you need to look at what entries were made in the register Calculations of taxpayers with the budget for personal income tax. For this:

- Select on the left the register Calculations of taxpayers with the budget for personal income tax;

- Click Add. The line from the Available commands section goes to the Selected commands section;

After such actions, you can see that a navigation panel has appeared in the form of the Vacation document, which always begins with the word “Main”, and then links to registers that will be added to the selected commands are listed. In the example it would look like this:

By clicking on this command you can see the entries made in the register:

You can return to the document form by clicking Main.

Similarly, any registers from the list of available commands in the form navigation settings for any documents are added. You just need to remember that for this setting the document must be open.

So, let's see what records on the movement of personal income tax in 1C 8.3 ZUP 3.0 were formed with the Vacation document status “Passed”.

Accumulation register “Accounting for income for calculating personal income tax”

This register contains information:

- about the amount of income in the context of income codes - comes from the calculation of vacation received on the Accrued tab:

- date of receipt of income - recorded in the register from the value of the document details Date of payment on the Main leave tab:

- and month of the tax period - from the Month attribute in the document header:

The information contained in this register corresponds to the calculated personal income tax. An entry in this register is formed with a “+” sign (arrival):

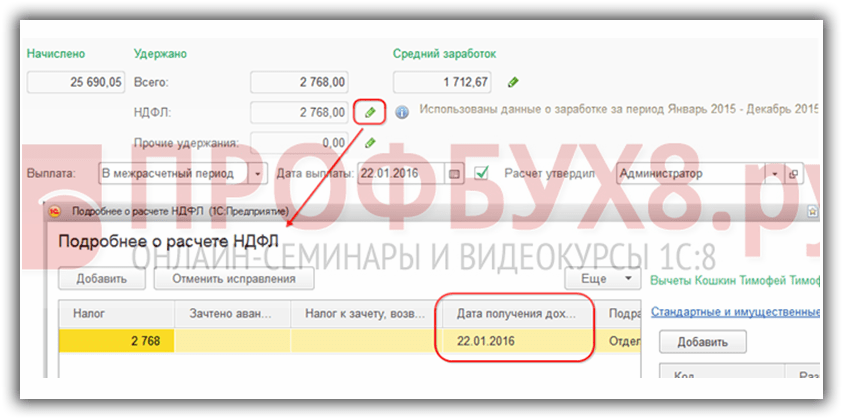

The personal income tax amount is stored in the following sections:

- date of receipt of income - enters the register from the details of the date of receipt of income, located in the details of personal income tax calculation:

- tax rates;

- registration with the Federal Tax Service - in our example, we take the Federal Tax Service with which the organization itself is registered.

Accumulation register “Provided standard and social deductions (NDFL)”

Entries in this register indicate that the employee is entitled to deductions and they were provided to him with this document:

What you need to pay attention to when registering the “Vacation” document for correct personal income tax accounting is “Document date” detail(in our example, 01/19/2016) As can be seen from the illustrations, this date passes through all of the listed registers as the “Period” attribute.

How personal income tax is withheld upon payment

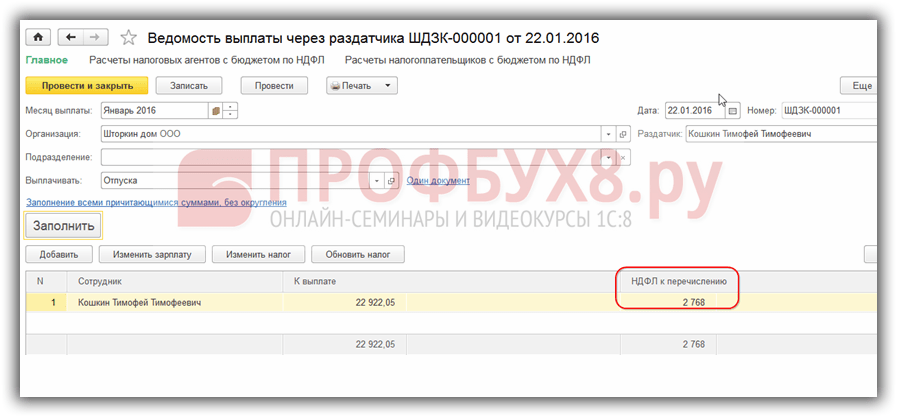

In our example, salary payment is made through the distributor, so we will generate the document Statement of payment through the distributor:

- Select the month of payment – January 2016;

- The date of the document must correspond to the date of payment, for example it is 01/22/2016;

- We indicate that we pay vacation;

- Using the “Not selected” link, select which vacation we pay for;

- Finish by clicking Select:

When filling out the document, in 1C ZUP 3.0 the amount to be paid and the amount of personal income tax to be transferred are automatically set:

If you slightly change the data in the document, for example, change the date of the document, the picture will be completely different - the personal income tax for the transfer is not filled out in the tabular section:

The question arises: Why is personal income tax not filled out for the transfer? It turns out that the date of the document is very important, that is, the date when the payment is generated. Personal income tax, which arose when calculating vacation, was formed on the date January 19, 2016. and, accordingly, cannot be listed earlier than this date, that is, it is simply not in the 1C ZUP 8.3 database yet. Records with this personal income tax appear in all registers only from January 19, 2016.

How to view entries in accumulation registers upon payment

The document that forms the payment also makes movement through the registers associated with personal income tax.

Accumulation register “Calculations of taxpayers with the budget for personal income tax”

The entry that the payment generates is formed in the register with the sign “-” (expense) and such personal income tax is considered withheld.

The amount of withheld personal income tax is stored in the following sections:

- date of receipt of income is the date of receipt of income, which can be viewed in the details of personal income tax calculation of the Vacation document itself;

- tax rates;

- registration with the Federal Tax Service.

It is the data on the withheld tax that then falls into the 6-NDFL reporting:

Accumulation register “Calculations of tax agents with the budget for personal income tax”

We see that two entries were made to this register:

- + (“receipt”) - withheld personal income tax;

- – (“expense”) – listed personal income tax:

Since 2011, a number of changes introduced to Chapter 23 of the Tax Code of the Russian Federation by Federal Law No. 229-FZ of July 27, 2010, have come into force. In particular, starting from 2011, tax agents are required to keep personal income tax records in tax accounting registers, the forms of which are proposed to be developed independently. In the program "1C: Salaries and Personnel Management 8" (release 2.5.32) the tax register form has already been implemented. E.A. talks about the new form and changes related to the accounting and calculation of personal income tax. Gryanina, independent consultant.

paragraph 1 of article 230 of the Tax Code of the Russian Federation

Tax amount calculated

Amount of tax withheld

Tax amount transferred

.

In the register Calculations of tax agents with the personal income tax budget Coming Consumption Transfer of personal income tax to the budget.

List of documents Transfer of personal income tax to the budget of the Russian Federation can be called from the menu Taxes and contributions -> Transfer of personal income tax to the budget of the Russian Federation Taxes, paragraph Transfer of personal income tax to the budget of the Russian Federation(see Fig. 1).

Rice. 1

In the header of the document Transfer of personal income tax to the budget of the Russian Federation

In the tabular section Employees Fill in -> Individuals

Fill in -> Tax amounts

When posting a document Transfer of personal income tax to the budget of the Russian Federation Calculations of tax agents with the personal income tax budget.

Accounting for transferred personal income tax amounts for each taxpayer

The form of the tax register for personal income tax is not regulated by law, however, the new version of paragraph 1 of Article 230 of the Tax Code of the Russian Federation lists information that must be contained in the tax register. The composition of this information has been expanded compared to the data in Form 1-NDFL, which was used previously. In particular, now tax agents must additionally take into account the amounts of personal income tax actually transferred for each individual, indicating the date of transfer and details of the payment document. This amount will also need to be indicated in the information on the income of individuals in Form 2-NDFL for 2011. Thus, since 2011, tax agents must take into account three tax amounts for each individual:

Tax amount calculated- how much tax was assessed to be withheld from the income of an individual;

Amount of tax withheld- how much tax was actually withheld when paying income to an individual;

Tax amount transferred- how much tax was actually transferred to the budget system.

To register the amounts of the transferred tax in the program "1C: Salary and Personnel Management 8" a new document has been created Transfer of personal income tax to the budget of the Russian Federation. To record the amounts subject to transfer and actually transferred to the budget for each individual - a new accumulation register Calculations of tax agents with the personal income tax budget.

In the register Calculations of tax agents with the personal income tax budget with a "+" sign (by type of movement Coming) the amounts of tax withheld from individuals, subject to transfer to the budget, are reflected with a “-” sign (by type of movement Consumption) - transferred tax amounts. The balance in the register shows the amount of tax withheld from employees, but not yet transferred to the budget - it is this data that is used to automatically fill out the program document Transfer of personal income tax to the budget.

Please note that the document date and payment date must be no earlier than the first day of the month following the billing period.

After updating the program version, it is necessary to register the transfer of personal income tax in the information database in relation to all income received by taxpayers starting from 01/01/2011. It is recommended to register personal income tax transfer upon payment.

List of documents Transfer of personal income tax to the budget of the Russian Federation can be called from the menu Taxes and contributions -> Transfer of personal income tax to the budget of the Russian Federation or from the program desktop: bookmark Taxes, paragraph Transfer of personal income tax to the budget of the Russian Federation(see Fig. 1).

Rice. 1

Personal income tax transfers are registered in the program separately for each month of the tax period, for each tax rate and OKATO+KPP code.

In the header of the document Transfer of personal income tax to the budget of the Russian Federation you should indicate: the date of payment, the month of the tax period for which the tax was transferred, details of the payment order for payment of the tax, the tax rate, in the case of separate divisions - specify the OKATO/KPP code, and enter the total amount of the transferred tax at this tax rate and code OKATO/KPP.

In the tabular section Employees- indicate how much tax was transferred for each specific taxpayer. The list of employees can be filled in automatically by command Fill in -> Individuals who received income. The list will include all individuals for whom tax amounts for transfer are registered in the program. The amount for each individual will be calculated by proportional distribution of the total amount indicated in the header of the document. If necessary, the amounts in the tabular section can be adjusted manually. The total tax amount for all taxpayers must coincide with the amount indicated in the header of the document.

If the list of employees in the document is selected manually, then the command is used to distribute the total tax amount between employees Fill in -> Tax amounts(allows you to fill out tax amounts without refilling the list of individuals).

When posting a document Transfer of personal income tax to the budget of the Russian Federation the amounts of transferred tax for each individual indicated in the tabular part are recorded in the accumulation register Calculations of tax agents with the personal income tax budget.

The distribution is made in proportion to the amount of tax to be transferred for each individual (the balance according to the accumulation register Calculations of tax agents with the budget for personal income tax). For example, if, for some reason, only 50% of the total amount of personal income tax withheld from employees is paid to the budget, then for each individual a transfer of half the amount of tax withheld from him will be registered.

Tax accounting register for personal income tax

To compile a tax accounting register for personal income tax, a new report has been added to the program Tax accounting register for personal income tax. The report can be called using the submenu item of the same name Taxes and fees or from bookmarks Taxes program desktop.

Using this report, you can generate tax accounting registers for personal income tax for the selected tax period for all employees of the organization at once or only for a selected list of individuals.

The personal income tax register form implemented in the program fully complies with the requirements for the composition of information specified in paragraph 1 of Article 230 of the Tax Code of the Russian Federation. Let us recall that in accordance with paragraph 1 of Article 230 of the Tax Code of the Russian Federation, the tax register must contain information that allows identification of the taxpayer, the type of income paid to the taxpayer and tax deductions provided in accordance with established codes, the amount of income and the date of their payment, the status of the taxpayer, the dates of withholding and tax transfers to the budget system of the Russian Federation, details of the corresponding payment document.

The Register includes 7 sections.

Section 1 contains information about the tax agent.

Section 2 contains information about the taxpayer (recipient of income). Paragraph 2.9 provides information about the tax status of the taxpayer in table form. For designation, the same taxpayer status codes are used as for form 2-NDFL: 1 - tax resident, 2 - non-resident, 3 - highly qualified foreign specialist.

Section 3 provides information about a taxpayer's right to standard tax deductions. This information is filled in based on the deduction data specified for the individual in the form Entering data for personal income tax(see Fig. 2).

Rice. 2

Section 4 provides information on the calculation of the tax base and personal income tax. Section 4 is formed separately for each OKATO/KPP code. If during the tax period an employee worked and received income in various separate divisions, then the Register of this employee will contain several sections 4. Section 4 consists of several subsections.

Subsection Calculation of personal income tax at the rate of __% is formed separately for each tax rate. In the subsection, by month of the tax period, the codes and amounts of income received by the taxpayer, the amount of taxable income and calculated tax are given. For income taxed at a rate of 13%, an additional table is displayed with information about the tax deductions actually provided to the taxpayer.

In subsections Tax calculated, Tax withheld And Tax transferred The amounts of calculated, withheld and transferred tax are given accordingly by month of the tax period and tax rates. A separate column indicates the date of the transaction: calculation, deduction, transfer of tax. For the amounts of the transferred tax, details of the payment order are additionally displayed (see Fig. 3).

Rice. 3

Section 5 indicates the total amounts of tax deductions actually provided to the taxpayer for the tax period as a whole. The information is displayed in the context of OKATO/KPP codes and deduction codes.

Section 6 provides the total amounts of income and tax based on the results of the tax period, broken down by OKATO/KPP codes and tax rates.

Section 7 specifies information about the submission of taxpayer income certificates in Form 2-NDFL.

Changes in the calculation of personal income tax related to changes in the Tax Code of the Russian Federation

Since 2011, the procedure for calculating personal income tax for individual cases has changed.

Newly in 2011, tax is calculated in case of providing an employee with property deductions. The changes apply to the month from which the deduction begins to apply. In accordance with the new edition of Article 220 of the Tax Code of the Russian Federation, property tax deductions are provided for employee income received starting from the month the employee submitted an application for such a deduction. Previously, the deduction was provided for income from the beginning of the tax period, regardless of the month in which the employee submitted the application. When calculating personal income tax in the month of submission of the application, the program recalculated the tax from the beginning of the year, and it was possible to return or offset the amount of tax on income for previous months. In 2011, tax recalculation for the months of 2011 preceding the month the employee submitted the application is not performed.

In addition, the procedure for calculating tax when an employee acquires the status of a tax resident of the Russian Federation has changed. In accordance with the new edition of Article 231 of the Tax Code of the Russian Federation, recalculation and refund of tax when a taxpayer acquires tax resident status is carried out by the tax inspectorate itself. Previously, the tax agent could recalculate and return the tax in this case, so the program recalculated the tax at a rate of 13% for the entire tax period. In 2011, when an employee acquires the status of a tax resident of the Russian Federation, the tax from the beginning of the year is not recalculated, but begins to be calculated at a rate of 13% from the month of change of status.

Examples of tax calculation for these cases are discussed in the ITS reference book “Maintaining personnel records and settlements with personnel in 1C programs.”

Change in personal income tax calculation related to the personal income tax calculation subsystem

Let us note one more change in the program related to the personal income tax calculation subsystem. The location where information about an employee's tax status is entered has changed. Previously, input was carried out in the form of entering data on the citizenship of an individual. Now the taxpayer status is indicated on a special page of the form Entering data for personal income tax(called from the individual’s data form using the button Personal income tax, or from the field Status directory Employees) - see fig. 4.